Gold prices fell as investors sold bullion to raise cash during an Iran-driven liquidity crunch, but Saxo Bank says the outlook for gold could improve quickly once forced selling fades. For Indian investors, that means near-term volatility in global XAUUSD may still spill into domestic gold rates, especially if the U.S. dollar, Treasury yields, and crude oil remain elevated.

Why is gold price falling despite safe-haven demand?

Gold price is falling because investors are liquidating profitable positions to raise cash, even as geopolitical risk remains high. According to Ole Hansen, Head of Commodity Strategy at Saxo Bank, the selloff reflects a liquidity squeeze triggered by the Iran conflict rather than a collapse in gold’s long-term investment case.

Hansen said gold and silver remain under considerable pressure as the Middle East war triggers a broad macroeconomic shock across global markets. He wrote that investors are being forced to reprice inflation, interest rates, growth, and liquidity conditions all at once.

He added that both precious metals had delivered many months of strong outperformance, which left them vulnerable when markets suddenly needed liquidity. In his view, gold’s strategic case has not fundamentally changed, but the trade had become crowded on the long side.

Hansen said gold is being sold because it remains one of the few liquid assets still showing gains over the past year. That has made bullion a source of cash for investors facing margin pressure, stop-loss triggers, and broader deleveraging.

For Indian investors, this kind of global liquidation can temporarily push domestic gold prices lower even when geopolitical tensions would normally support safe-haven buying. However, rupee weakness against the U.S. dollar can cushion or even offset part of any global decline in local bullion prices.

How is the Iran conflict creating a liquidity crunch in precious metals?

The Iran conflict is tightening liquidity by driving a wider macro shock through energy markets, inflation expectations, and funding conditions. Hansen said the market is reacting not only to war risk but also to what may be the largest disruption to global fuel supply on record.

He said equity markets have been selling off as growth concerns rise, while funding costs and bond yields surge on mounting inflation fears. Hansen argued that with limited remaining conventional military capacity, Iran is delivering a broad retaliatory shock through energy markets, and the spillover effects are widening globally.

That matters for gold because a sharp rise in oil and energy prices can create a stagflationary backdrop. In the short run, however, traders often sell gold and silver to meet cash needs elsewhere in their portfolios.

What do rising U.S. yields mean for bullion?

Rising U.S. yields are adding pressure to bullion because they increase the opportunity cost of holding non-yielding assets like gold. Hansen noted that the U.S. 2-year Treasury yield moved above the Federal Reserve's fed funds rate for the first time in three years on Friday.

He said that move signals a growing likelihood that the Federal Reserve’s next step could be a rate hike rather than further easing. A more hawkish Fed outlook typically supports the U.S. dollar and weighs on XAUUSD in the near term.

For Indian gold buyers, higher U.S. yields can affect imported gold prices through both global bullion benchmarks and currency moves. If the dollar strengthens while the rupee weakens, domestic gold prices may remain firm even when spot gold retreats.

What technical levels is Saxo Bank watching for gold and silver?

Saxo Bank says the selloff has turned technically significant, with gold returning to its 200-day moving average for the first time since 2023. Hansen said that move highlights the scale of the reversal now underway in precious metals.

He described gold as one of the more exposed assets in the current environment because the selloff is being driven by long liquidation, stop-loss selling, and urgent demand for liquidity. That combination often creates outsized price swings in a short period.

Why is silver under even more pressure than gold?

Silver is under more pressure because it has higher beta and greater sensitivity to the economic cycle. Hansen said silver could have further to fall than gold if growth fears keep intensifying.

He said the selloff accelerated after silver broke below USD 80, which from a technical perspective opened the way toward USD 40. Since then, the unwind of previously popular trades has added more downside momentum.

Hansen noted that silver earlier on Monday almost reached the 0.618 Fibonacci extension target at USD 60.80. He said that level may offer initial support.

If silver fails to hold USD 60.80, Hansen identified the 200-day moving average at USD 57.61 as the next key downside level. For Indian investors tracking silver prices alongside gold, that signals continued volatility in the white metal.

How big is the current correction in gold and silver?

The correction is steep, with gold down more than 19% in March and silver down nearly 31. Hansen said the pullback looks dramatic, but it follows an unusually strong rally over the prior year.

On a one-year basis, gold remains up 38.3%, while silver is up 90.0%. Hansen said those gains show how strong the preceding rally had been and help explain why the current liquidation phase is proving so intense.

These figures matter for investors because strong prior gains often leave markets vulnerable to deeper corrections when leveraged positions unwind. In India, such moves can create sharp day-to-day swings in gold and silver rates, especially when global risk sentiment deteriorates.

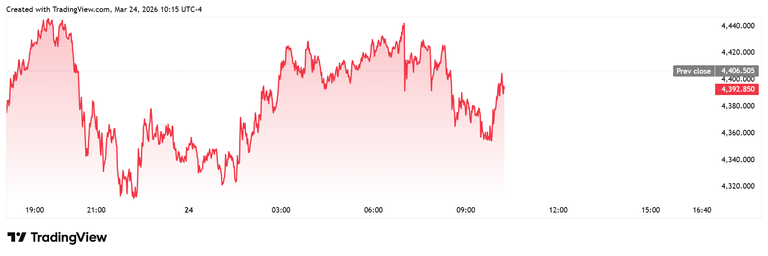

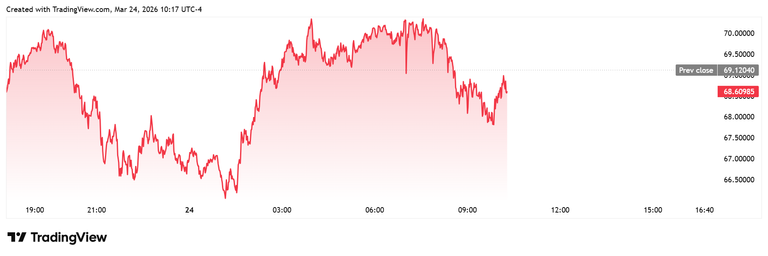

Where are gold and silver trading now?

At the time of writing, spot gold was trading in the middle of its daily range at $4,392.26 per troy ounce, down 0.32% on the session. Silver was last trading at $68.606 per ounce, down 0.74% on the daily chart.

Those intraday levels show that both metals remain volatile as traders balance safe-haven demand against liquidity stress, higher yields, and broad macro uncertainty.

Why does Saxo Bank expect gold outlook to improve sharply later?

Saxo Bank expects the gold outlook to improve sharply once forced selling runs its course. Hansen said that after the dust settles, gold in particular could recover because the underlying macro drivers remain supportive.

He pointed to growing fiscal debt concerns, rising stagflation risks, and the threat that higher energy costs will weaken growth while keeping inflation elevated. In that environment, policymakers have limited flexibility, which could renew demand for gold as a hedge against macro instability and currency debasement.

Hansen also tied the longer-term case to de-dollarization and fiscal stress. Those themes continue to support strategic demand for bullion even if short-term market moves remain disorderly.

Will silver rebound too?

Silver may rebound as well, but Hansen said it is likely to remain more sensitive to growth concerns in the near term. That makes silver potentially more volatile than gold until markets gain confidence that the economic shock is easing.

For Indian investors, the key watchpoints now are U.S. Treasury yields, Federal Reserve expectations, crude oil prices, and rupee-dollar moves. If forced liquidation eases while stagflation fears keep building, global gold price trends could turn higher again quite sharply, with direct implications for Indian bullion and jewellery markets.