# Gold Price Rally: CME Says US Dollar Is the Key Driver

Gold prices and the wider commodity complex have rallied on geopolitics, central bank buying, fiscal and monetary policy, and rising industrial demand for silver, but CME Group says the U.S. dollar remains the single most important driver. For Indian investors, that matters because moves in the dollar affect global bullion prices, XAUUSD trends, and the rupee cost of imported gold.

What is driving the gold price rally and the broader commodity surge?

The answer is that several forces are pushing commodities higher at once, but they do not affect every sector equally. According to Dr. Mark Shore, director and economist at CME Group, the last 14 months have delivered a historic performance for global commodities.In a new analysis published Monday, Shore said investors coming out of the first quarter of 2026 are navigating "a complex web of geopolitical tensions, currency fluctuations and shifting supply-demand cycles." He said understanding the current market requires looking beyond headline price moves to the hidden drivers underneath them.

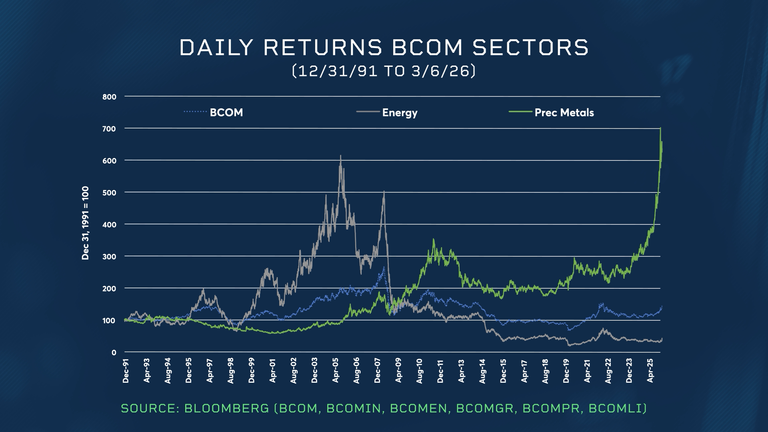

Shore stressed that commodities do not move as one block. Using the Bloomberg Commodity Index, or BCOM, and its five commodity sectors as a proxy, he said commodity markets tend to be mean-reverting and cycle between expansion and contraction as supply and demand shift.

For gold and other precious metals, the current rally has been driven by increased geopolitical tensions, fiscal and monetary policies, central banks continuing to accumulate gold, and strong industrial demand for silver. Shore said silver demand has been boosted by the energy transition and by data center construction.

For Indian investors, this is especially relevant because India is one of the world’s largest gold-consuming markets. A rise in global bullion prices, especially when paired with rupee weakness against the U.S. dollar, can quickly lift domestic gold rates.

Why does CME say the U.S. dollar matters most for commodities?

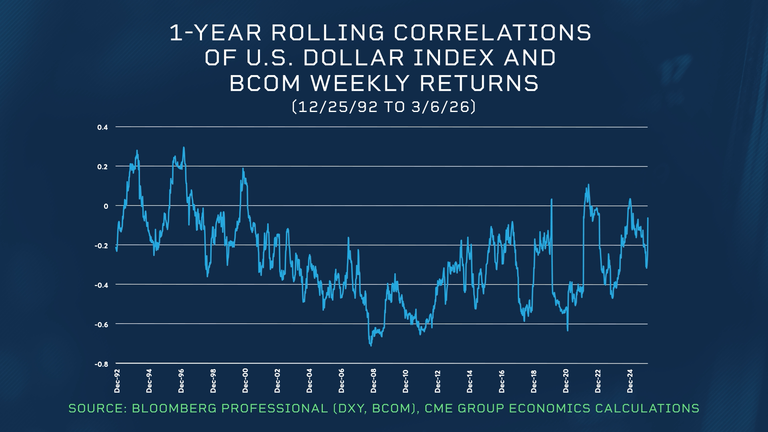

The answer is that most commodities are priced in dollars, so currency moves directly affect global demand. When the U.S. dollar weakens, commodities become cheaper for buyers using other currencies, which usually encourages more buying.Shore called the greenback the single most important catalyst for the Bloomberg Commodity Index and all of its sectors. He said, "Perhaps no relationship is more important for commodity investors than the influence of the U.S. dollar."

He backed that view with long-term data. Between January 1992 and March 2026, the correlation of weekly returns between the U.S. Dollar Index, or DXY, and BCOM was -0.31, showing an inverse relationship 89% of the time on a 12-month rolling basis.

That inverse relationship matters for gold price forecasting. A softer dollar often supports gold, silver, and broader commodity prices, while a stronger dollar can weigh on XAUUSD and other raw materials.

For Indian buyers, the impact can be mixed. If global gold rises because the dollar weakens, that can support international bullion prices. But if the rupee also weakens against the dollar, Indian gold prices may rise even faster in INR terms.

How have past commodity rallies compared with the current precious metals rally?

The answer is that earlier cycles were led by energy, industrial metals, and grains, while the latest cycle has been led by precious metals. Shore used earlier BCOM moves to show how leadership changes over time.How strong was the early-2000s energy rally?

The energy sector rallied more than 860% between February 1999 and September 2005, leading the Bloomberg Commodity Index. Shore said that move was driven by structural demand growth from China and India, along with supply shocks from Iraq and Venezuela.

A second energy rally followed from January 2007 to July 2008. That move pushed WTI crude oil above $147 per barrel as global demand remained firm, supplies stayed tight, geopolitical tensions persisted, and the U.S. dollar weakened.

What happened in industrial metals and agricultural markets?

The industrial metals sector rallied about 395% from November 2001 to May 2007. Shore said China’s industrialization and urbanization drove that advance.At the same time, grain markets saw several rallies between 2002 and 2012. Those gains were influenced by a weaker U.S. dollar, the growth of biofuels, and rising global demand for animal products.

Why are precious metals leading now?

The precious metals sector has taken the lead in recent years. Shore said the current surge has been fueled by increased geopolitical tensions, fiscal and monetary policies, central bank gold accumulation, and industrial demand for silver tied to the energy transition and data centers.That combination is important for Indian investors because it supports both investment demand for gold as a safe-haven asset and strategic interest in silver as an industrial precious metal.

What other commodity sectors are rising besides gold and silver?

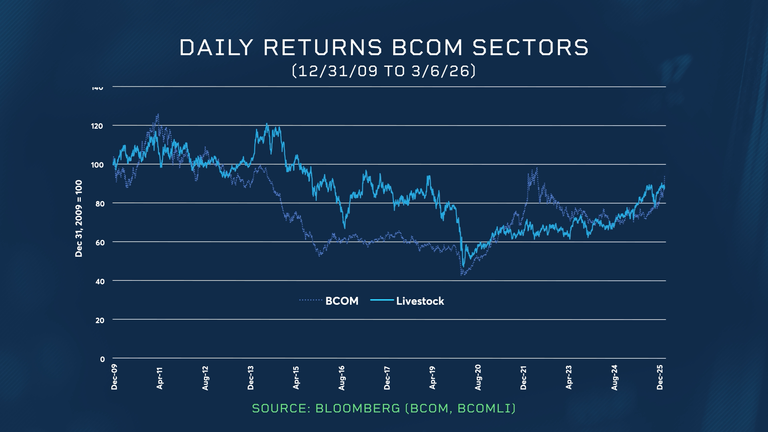

The answer is that gains have not been limited to bullion and energy. Shore said the BCOM livestock sector, especially live cattle, has also moved higher since 2020.From April 2020 to March 2026, the livestock sector appreciated 86%. He said that gain was driven mainly by the smallest herd size since 1951 and the strongest consumer demand in the past two decades.

This broader participation across commodity sectors suggests the current cycle is not just a narrow gold price story. It reflects deeper supply constraints, demand shifts, and macroeconomic forces moving across the raw materials complex.

How does inflation connect to commodity prices?

The answer is that commodity prices can influence inflation, but the effect is usually delayed rather than immediate. Shore said many investors oversimplify the relationship between raw material prices and consumer inflation.Because commodity indices track inputs at the early stages of the supply chain, price changes take time to reach households. Shore said it can take several months for moves in commodity markets to fully show up in inflation indices that measure what consumers actually pay.

That lag matters for portfolio strategy and inflation hedging. Shore said the effect is particularly important in an environment where central banks remain highly focused on inflation signals.

For Indian investors, this has two implications. First, rising commodity prices can eventually feed into imported inflation, especially in an economy sensitive to energy and raw material costs. Second, gold can remain attractive as a hedge when inflation risks stay elevated and monetary policy remains in focus.

What should Indian gold investors watch next?

The answer is that Indian investors should closely track the U.S. dollar, central bank policy, geopolitical tensions, and physical demand trends in gold and silver. According to Dr. Mark Shore, commodity sectors can move independently, but their correlations can also shift between positive and negative phases.He concluded that whether the driver is the U.S. dollar, monetary policy, geopolitical risk, or a supply-demand imbalance, investors need to understand the hidden forces behind market moves. For India, the next key watchpoint is how global bullion prices interact with the rupee, because that combination will shape domestic gold price trends as 2026 unfolds.