# Gold Price Outlook Stays Bullish as HSBC Flags Stagflation Risks

Gold prices remain bullish over the medium to long term even without Federal Reserve rate cuts, according to HSBC. The bank says stagflation risks, rising fiscal deficits, geopolitical tensions and central bank buying should continue to support bullion, despite sharp short-term volatility in 2026.

Rodolphe Bohn, FX and Commodities Strategist at HSBC, said gold started 2026 with extreme swings. Gold fell from $5,415 per ounce in late January to $4,400 by March 26 as the conflict with Iran intensified and investors rushed into the U.S. dollar.

For Indian investors, the message is important: global gold price volatility in XAUUSD can still translate into a supportive long-term backdrop for domestic bullion, especially if geopolitical risk stays elevated and fiscal stress keeps demand for safe-haven assets firm. Any move in the U.S. dollar and crude oil also matters for India because it affects the rupee, imported inflation and local gold prices in INR.

Why does HSBC still see a bullish gold price outlook?

HSBC still sees a bullish gold price outlook because medium-to-long term drivers remain supportive even after the recent correction. The bank points to geopolitical risk, rising global debt, stagflation fears and expected improvement in central bank demand.

Bohn said the recent Middle East conflict increased short-term volatility, but it did not damage the broader investment case for gold. He argued that elevated fiscal deficits and concerns about financial stability are pushing investors toward hard assets such as gold.

HSBC also expects these structural drivers to persist. According to Bohn, they are unlikely to reverse in the medium term, which should keep underlying support in place for bullion prices.

What happened to gold prices in early 2026?

Gold was highly volatile at the start of 2026. Prices dropped from $5,415 per troy ounce in late January to $4,400 by March 26 as the conflict with Iran escalated.

That move showed that gold did not act as a simple geopolitical hedge during the risk-off phase. Instead, investors sold bullion to raise liquidity while the U.S. dollar captured most of the safe-haven demand.

Why does this matter for Indian investors?

This matters for Indian investors because domestic gold prices do not move only on fear headlines. Indian bullion rates also react to the U.S. dollar, Treasury yields, crude oil and the rupee.

If the U.S. dollar strengthens sharply, it can pressure international gold even during geopolitical stress. But for India, a weaker rupee and higher oil prices can cushion or even amplify local gold prices, making the INR gold trend different from the global dollar price move.

What drove gold prices lower during the Iran conflict?

Gold prices fell during the Iran conflict because investors preferred liquidity and the U.S. dollar over bullion. According to HSBC, oil prices surged, the U.S. dollar strengthened, yields rose and equities fell during the risk-off phase.

Bohn wrote, “During this risk-off phase, oil prices surged, the US dollar strengthened as the market’s preferred safe-haven assets, yields rose, and equities fell.” He added that “Gold did not act as a straightforward ‘geopolitical hedge’, as investors sold bullion to raise liquidity while the US dollar absorbed most of the safe-haven demand.”

That distinction matters. In some crises, gold rallies immediately as a safe-haven. In this episode, the stronger U.S. dollar and the need for cash overwhelmed that traditional response.

Did gold recover after the ceasefire?

Yes, gold rebounded quickly after the ceasefire helped calm markets. Bohn said the latest de-escalation showed that gold can recover fast as broader market conditions stabilise.

This suggests that gold’s short-term declines may be driven more by cross-asset stress and dollar strength than by a breakdown in its long-term safe-haven role. For traders in XAUUSD, that means geopolitical shocks can create sharp two-way moves rather than a one-direction rally.

How do oil prices and the U.S. dollar affect gold?

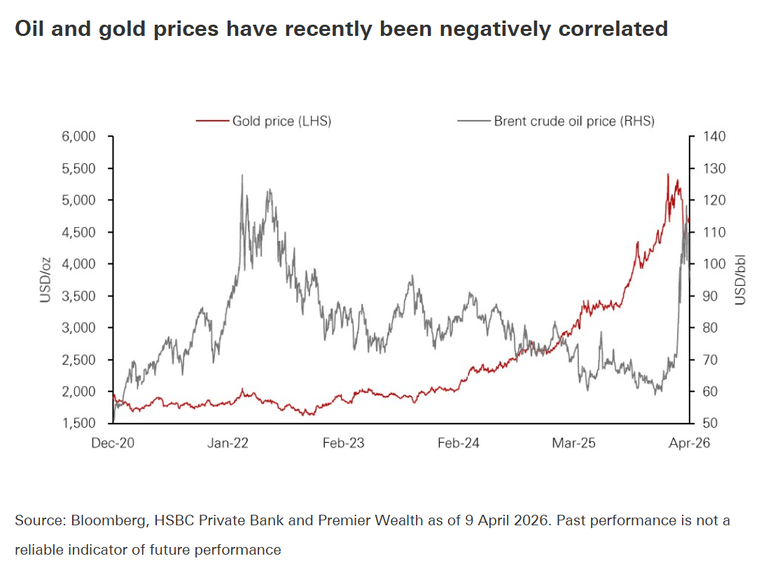

Oil prices and the U.S. dollar affect gold in different ways, and the relationship can change quickly depending on the shock. HSBC said gold and oil had a clear positive correlation before the conflict, but that relationship later neutralised as the two commodities moved in opposite directions.

Bohn explained that a stronger U.S. dollar usually pressures both gold and oil. But in this case, the Middle East supply shock pushed oil prices higher even as the U.S. dollar rally weighed on gold.

He said, “In the current market environment, a strong rise in oil prices does not necessarily trigger the same dynamics in gold prices.” In other words, higher crude alone is no guarantee of a higher gold price.

Why is this especially relevant for India?

This is especially relevant for India because the country imports most of its crude oil and gold. Higher oil prices can widen inflation pressures and strain the rupee, while a stronger U.S. dollar can influence both imported costs and investor sentiment.

For Indian households and investors, that means domestic gold prices may remain resilient even when global bullion struggles. A combination of rupee weakness, higher energy costs and safe-haven demand can keep local prices elevated.

How do Federal Reserve policy and stagflation risks affect gold?

Federal Reserve policy still matters for gold, but HSBC does not think rate cuts are necessary for prices to stay supported. The bank expects Fed policy rates to remain unchanged through 2026 and 2027, yet still sees stagflation risks as a positive driver for bullion demand.

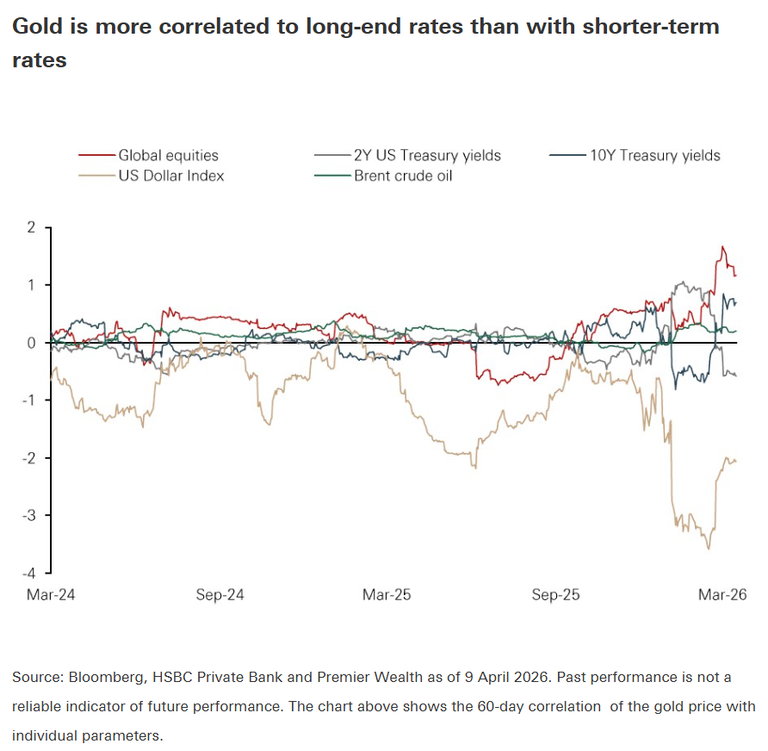

Bohn said high real yields can be a headwind because gold offers no yield. He noted that long-end rates have become more important since the conflict began, moving alongside a stronger U.S. dollar, weaker equities and higher oil prices.

Even so, HSBC believes stubborn inflation and rising threats to growth can support gold. That is the classic stagflation setup: weak growth combined with persistent inflation, a backdrop that often boosts demand for safe-haven and hard assets.

What is HSBC’s Fed view?

HSBC expects the Federal Reserve to keep policy rates unchanged through 2026 and 2027. That could limit some upside in gold, but the bank does not see it as enough to derail the broader bullish trend.

Bohn said, “Although we still expect Fed policy rates to remain unchanged through 2026 and 2027, which could limit gold’s upside, stagflation risks should continue to support demand for gold.”

For Indian investors, this means watching U.S. yields closely. If long-end yields ease while inflation concerns remain sticky, gold could gain fresh support globally and in the Indian market.

Why do fiscal deficits and debt levels support gold prices?

Rising fiscal deficits and debt levels support gold because they increase demand for hard assets when investors worry about financial stability. HSBC sees this as one of the strongest long-term pillars for bullion.

Bohn said growing debt burdens in the United States and other countries are pushing investors toward gold. He cited IMF estimates showing U.S. debt close to 100% of GDP in 2025.

He also said higher defence spending globally is adding to debt burdens. In HSBC’s view, these fiscal pressures are unlikely to reverse in the medium term, which should keep long-run support under gold prices.

Why should Indian investors track global debt trends?

Indian investors should track global debt trends because they shape currency markets, inflation expectations and appetite for safe-haven assets. When confidence in fiscal discipline weakens, investors often turn to bullion as a store of value.

That can reinforce the case for strategic gold allocation in Indian portfolios, especially during periods of market stress, rupee volatility or inflation uncertainty.

Will central bank gold buying continue to support prices?

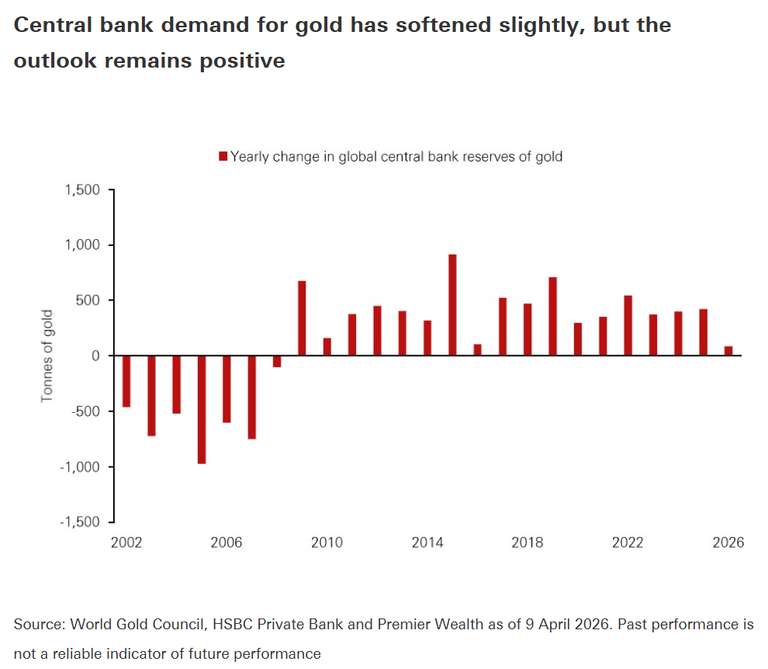

Yes, HSBC expects central bank gold buying to improve later in the year, even though demand has cooled from earlier peaks. The bank said official-sector buying remains an important long-term support for bullion.

Bohn noted that central bank demand has eased from the high levels seen between 2022 and 2024. He also said some central banks have sold gold to preserve foreign exchange reserves amid higher energy import bills and defence spending.

Still, HSBC expects long-term reserve diversification to reassert itself. Bohn said central bank demand should improve later in the year as diversification policies regain momentum.

What does central bank demand mean for bullion markets?

Central bank demand matters because it creates a steady source of structural buying in the gold market. Unlike short-term speculative flows, official-sector purchases often reflect long-term reserve strategy.

That makes central bank buying particularly relevant during periods when ETF inflows, coin demand or retail participation are softer.

How are high gold prices changing jewelry, coin and bar demand?

High gold prices are weakening jewelry and coin demand, while institutional demand for large bars has held up better. HSBC said elevated prices are changing both physical demand and supply across the bullion market.

Bohn said jewelry demand has been hit particularly hard. He also noted that demand for coins remains weak.

At the same time, institutional demand for large bars has been firmer, supported by regulatory changes in markets such as India and China. That point is especially important for Indian investors because regulatory shifts can change how bullion demand appears across different product categories.

What is happening on the supply side?

Mine supply is expected to rise modestly, and recycling should also increase. HSBC said mine output is set to rise modestly in 2026–27, while high prices should mobilise more scrap into the market.

Bohn warned that these shifts leave more bullion available for investors to absorb. If investment demand remains weak for an extended period, that extra supply could cap rallies.

He added, however, that retail investor demand has recently become more significant for gold prices. That suggests individual buying interest could play a larger role in supporting the market if institutional flows remain uneven.

What should investors watch next for gold prices?

Investors should watch Middle East de-escalation, the Strait of Hormuz, oil prices, inflation fears and bond yields. HSBC said the near-term direction of gold depends heavily on whether regional tensions continue to ease.

Bohn pointed to three key conditions: a ceasefire that persists or develops into a complete cessation of hostilities, the formal reopening of the Strait of Hormuz, and oil prices stabilising at lower levels. He said these conditions would reduce financial stress, ease inflation fears and support lower yields.

If that happens, gold could benefit from a more constructive macro backdrop rather than pure crisis demand. For Indian investors, the key watchpoint is whether lower oil prices and softer yields offset dollar moves and rupee fluctuations.

HSBC’s bottom line remains clear. Despite volatility and the absence of expected Fed rate cuts, the bank said, “We maintain a bullish view on gold over the medium-to-long term.”