# Gold Price Outlook: Merrill Sees Bullish Drivers Reasserting

Gold prices remain under near-term pressure, but Merrill says the long-term bull case for bullion is still intact. Emily Avioli, Vice President and Investment Strategist at Merrill, argues that the recent selloff reflects positioning, rising real yields and a stronger U.S. dollar—not a breakdown in gold’s structural demand story.

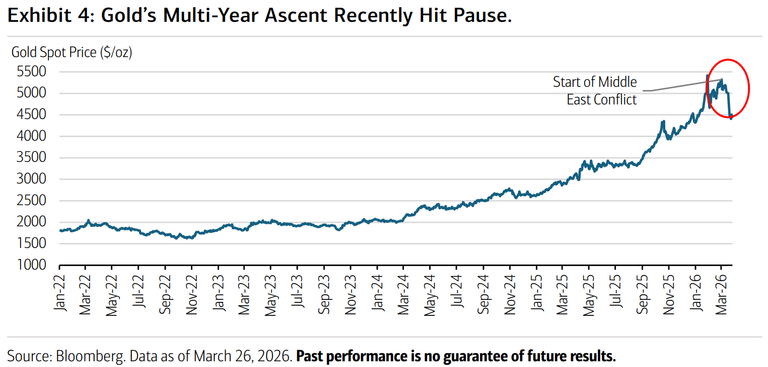

Why did gold prices fall despite the Iran war and rising inflation?

Gold prices fell because investors responded more to positioning, liquidity needs, interest rate expectations and U.S. dollar strength than to gold’s usual safe-haven role. According to Emily Avioli in Merrill’s latest Capital Market Outlook, gold has failed to outperform even as inflation rises and the Iran war unsettles investors.

Avioli said the move has been counterintuitive. She noted that gold prices have tumbled roughly 16.0% since the Middle East conflict began, even though geopolitical stress would normally support bullion.

She added that gold has moved largely in tandem with risk assets over the past four weeks. That means XAUUSD has not behaved like a classic geopolitical hedge during this phase of the conflict.

This unusual correlation has raised a key question for investors: should they be less bullish on bullion going forward? Avioli’s answer is effectively no, because the decline reflects market mechanics more than any deterioration in gold fundamentals.

What factors did Merrill say are pressuring gold in the near term?

Merrill said three forces are driving the pullback in gold: extended positioning after a huge rally, rising real yields, and a stronger U.S. dollar. These factors have created short-term headwinds for the gold price even as the broader long-term setup remains supportive.

How did positioning and profit-taking hit bullion?

Gold prices pulled back after an extraordinary rally, and Avioli said a consolidation phase is normal after such a sharp move. Supported by elevated central bank purchases and renewed retail enthusiasm, gold has surged since 2022 and recently moved above the $5,400 per ounce threshold in January.

Avioli said commodities often digest outsized gains after rapid rallies. In her view, that is exactly what has been happening in gold.

She also said market positioning had become increasingly extended after the historic run higher. When risk-off sentiment rose at the outbreak of the war, investors took profits in bullion.

Avioli added that some investors may have sold gold to raise liquidity. She said that move may have been amplified by depleted institutional cash on the sidelines, which had fallen to record lows in January.

How are rising yields hurting gold prices?

Rising yields are hurting gold because they increase the opportunity cost of holding a non-yielding asset. Avioli said higher energy prices have revived inflation concerns and changed the monetary policy outlook.

As a result, expectations for interest rate cuts have been pushed further out. She noted that fed funds futures now price in a non-trivial possibility that the Federal Reserve’s next move could potentially be a rate hike.

That shift matters for precious metals. As real yields rise, income-generating assets become more attractive relative to bullion, which does not pay interest.

Why is the U.S. dollar acting as a headwind for XAUUSD?

The U.S. dollar has strengthened since the conflict began, and that has pressured gold. Avioli wrote that investors have moved toward the dollar’s own safe-haven characteristics during the current crisis.

Gold has historically been seen as both a store of value and an alternative to the dollar. Because of that relationship, gold often moves inversely to the exchange-rate value of the U.S. dollar over recent decades.

When the dollar rises, XAUUSD typically faces resistance. That inverse relationship has been another major reason bullion has struggled in the current environment.

Why does Merrill still see long-term support for gold prices?

Merrill still sees long-term support for gold because the structural drivers behind the bull market have not disappeared. Avioli said none of the factors that helped push gold well above $5,000 per troy ounce have gone away.

She highlighted three main supports: lofty fiscal deficits, a likely return to U.S. dollar moderation, and ongoing central bank reserve diversification. These themes have underpinned gold in recent years and, in Merrill’s view, should continue to do so.

Avioli said central banks remain little incentivized to stop diversifying reserve assets. That matters because official-sector buying has been one of the strongest pillars of the global bullion market since 2022.

She also said the dollar is likely to resume its moderation trend over time. If that happens alongside persistent fiscal concerns, the backdrop for precious metals could improve again after the current war-driven dislocation fades.

What does this mean for Indian gold investors?

For Indian investors, Merrill’s view suggests that short-term gold price weakness may not invalidate the long-term investment case for bullion. Global moves in XAUUSD, U.S. Treasury yields and the dollar directly affect imported gold prices in India, while rupee moves can either cushion or amplify those effects.

If the U.S. dollar stays strong, Indian gold rates in INR may remain relatively firm even when international bullion prices correct. But if the dollar weakens later and structural gold demand reasserts itself, domestic prices could again find support from both global bullion strength and central bank buying.

Indian households also tend to view gold as both a store of value and a portfolio hedge. Merrill’s framing supports the idea that gold still has a role as a strategic diversifier in balanced portfolios, especially for investors managing inflation risk, currency volatility and geopolitical uncertainty.

For buyers in India, the key near-term watchpoints are U.S. real yields, Federal Reserve rate expectations, dollar direction and whether Middle East tensions begin to fade. If those headwinds ease, Avioli expects the underlying drivers of gold demand to reassert themselves.

What is Merrill’s portfolio view on gold now?

Merrill continues to support holding gold as a strategic diversifier. Avioli concluded that once uncertainty around the Middle East conflict starts to fade, the underlying demand drivers for bullion should re-emerge.

Her core message is that the recent decline does not mean investors should abandon gold. Instead, she sees the current weakness as a near-term consolidation after a major rally that took prices above $5,400/oz in January.

That distinction matters for investors tracking gold price outlooks. Near-term volatility may persist, but Merrill still sees a place for gold in balanced portfolios as fiscal risks, reserve diversification and long-term currency trends continue to support the metal.