# Gold Price Outlook: Gabelli Sees Powerful Path Above $6,000

Gold could rise above $6,000 per troy ounce in the medium term, according to Chris Mancini of Gabelli Funds, who argues that war in Iran, rising defence spending, and global de-dollarization are strengthening bullion's long-term appeal.

Mancini, co-portfolio manager of the Gabelli Gold Fund (GLDAX), told Kitco News on Tuesday that recent weakness in gold prices does not undermine the bullish case. Instead, he said the pullback shows gold is functioning as a liquid reserve asset during geopolitical stress.

Why does Chris Mancini still expect gold to rise above $6,000?

Gold remains bullish because fiscal strain, geopolitical conflict, and reserve diversification are all building a stronger medium-term case for higher prices.

Chris Mancini said gold was around $5,300 before pulling back amid selling pressure and related market factors. In his view, once the current turmoil settles and the broader global monetary shift becomes clearer, gold should move above $6,000 per ounce.

Mancini tied that outlook to more than just near-term safe-haven demand. He said the combination of the Iran war and rising defence spending in both Europe and the United States is creating conditions that typically support higher gold prices over time.

For Indian investors, that matters because any sustained rise in international XAUUSD prices can feed directly into domestic bullion rates, especially if the Indian rupee weakens against the U.S. dollar at the same time.

What is driving the current bullish gold price outlook?

The main drivers are the war in Iran, heavier defence spending in Europe and the U.S., and growing doubts about the long-term dominance of the U.S. dollar.

Mancini said the Iran conflict is supporting gold in a less obvious way than a simple price spike. He noted that some countries may be using gold reserves for liquidity rather than just holding them passively.

“Turkey as well as the Gulf states might be selling, especially if they’re unable to export their oil and need to cover their expenses,” Mancini said. “They have gold reserves, and gold is serving its purpose as a liquid asset right now.”

That point is important for bullion investors. Gold can face short-term selling during crises when governments or investors need cash, but that does not necessarily weaken the long-term thesis for precious metals.

How does de-dollarization support gold prices?

De-dollarization supports gold because countries looking to reduce dependence on the U.S. dollar need a reserve asset that does not rely on another government's promise to pay.

Mancini said the world is moving through a major shift in how global reserves are allocated. He linked that change partly to the fallout from Russia’s invasion of Ukraine, after which the United States froze or effectively confiscated Russian Treasury holdings.

According to Mancini, that event reshaped how many countries view sovereign reserves. He said Russia had effectively been lending to the United States by holding Treasuries, only to find those assets could be blocked.

“We’re going through a major paradigm shift in terms of the de-dollarization of global reserves,” Mancini said. “When Russia invaded Ukraine, the United States effectively confiscated the Treasuries that Russia owned, meaning Russia had been lending to the United States, and we essentially said we wouldn’t pay them back. That event helped drive gold from around $2,000 an ounce to about $5,000.”

He added that if surplus nations no longer want to keep recycling foreign exchange surpluses into dollars and U.S. Treasuries, gold could emerge as the primary alternative.

“If that’s the case, gold will become the primary alternative,” Mancini said.

For Indian investors, this reserve-shift theme matters because it supports structural central bank demand for bullion. Strong official-sector buying has been one of the key reasons gold prices have remained elevated globally.

Why does Mancini prefer gold over government bonds in this environment?

Mancini prefers gold because gold is a reserve asset with no counterparty risk, while government bonds depend on the credit and political reliability of the issuer.

He said gold differs fundamentally from U.S. Treasuries, German bonds, and French bonds because owning bullion does not mean lending money to a government.

“Gold is an asset that is no one’s liability,” Mancini said. “Unlike Treasuries, German bonds, or French bonds, you aren’t lending to anyone when you buy gold. When you purchase gold, you simply own it outright, but when you buy a Treasury, you’re lending to the United States government.”

He also warned that growing debts and deficits increase gold’s appeal. In his view, expanding defence budgets could add to those fiscal burdens and further strengthen the case for bullion.

“As debts and deficits grow, gold tends to become more attractive, which is one aspect of the trade right now,” he said. “Increased defense spending will likely contribute to that dynamic as well.”

This argument is especially relevant in India, where investors often buy physical gold and sovereign alternatives as long-term stores of value during periods of macro uncertainty, currency volatility, and inflation concerns.

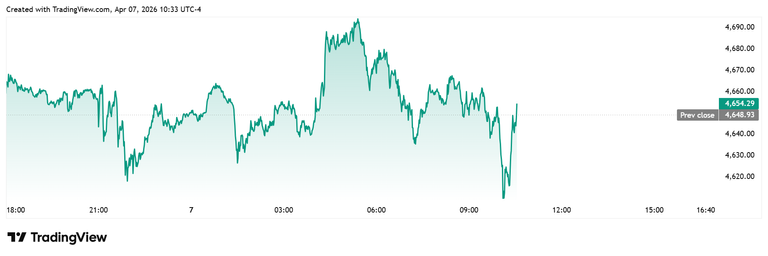

What happened to spot gold prices on Tuesday?

Spot gold stayed volatile on Tuesday, briefly falling to $4,607.72 per ounce before recovering to $4,653.72, up 0.10% on the session.

The spot gold price dipped to a session low shortly after 10 am EST as traders reacted to ongoing geopolitical developments and market selling pressure. It later recovered, showing that bullion remained supported even after the initial decline.

Kitco reported that spot gold last traded at $4,653.72 per troy ounce, a marginal gain of 0.10% on the day.

For Indian bullion buyers, such intraday XAUUSD swings can translate into rapid moves in local gold rates, depending on import costs, rupee-dollar moves, and domestic premiums.

What should Indian investors watch next in the gold market?

Indian investors should watch whether de-dollarization accelerates, whether defence spending rises further, and whether gold can regain and hold levels above $5,300 before targeting $6,000.

Mancini’s thesis is medium term, not just a reaction to a single headline from Iran. If reserve managers continue shifting away from dollar assets and fiscal deficits widen across major economies, gold could remain one of the most important safe-haven and reserve trades globally.

For India, the next key watchpoint is not only the international gold price but also the rupee’s direction. A stronger global gold market combined with INR weakness could amplify gains in domestic bullion prices even faster than international spot moves alone.