# Gold Price Outlook: Central Banks Sold Net 30 Tonnes in March

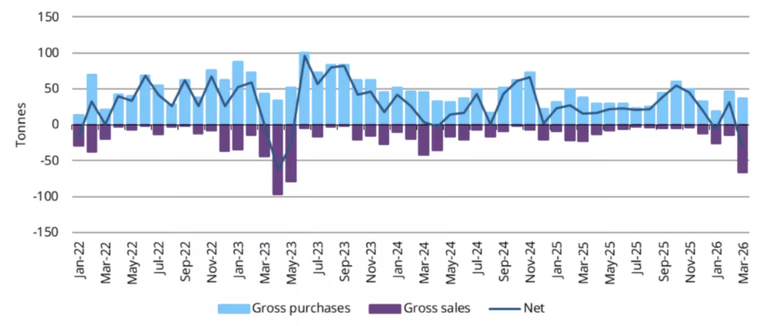

Central banks turned into net sellers of gold in March 2026, with 30 tonnes of net outflows, according to the World Gold Council. The shift matters for the gold price because official-sector buying has been one of the strongest pillars behind the multi-year bullion rally.

For Indian investors, this development is important because central bank demand influences global bullion sentiment, XAUUSD direction, and, ultimately, domestic gold rates when converted into rupees. Even when international gold prices stay firm, shifts in sovereign buying and selling can change near-term volatility in the Indian market.

Why did central banks become net sellers of gold in March 2026?

Central banks became net sellers in March 2026 mainly because Turkey sold 60 tonnes and Russia sold 16 tonnes, outweighing purchases by other official buyers. According to Marissa Salim, Senior Research Lead, APAC at the World Gold Council, sovereign demand flipped to the supply side in the final month of the first quarter.

Salim said on Tuesday that "central banks sold a net 30t of gold in March, with sales from Turkey (60t) and Russia (16t) offsetting purchases elsewhere." She also noted that quarterly data from the State Oil Fund of Azerbaijan (SOFAZ) showed net sales of 22 tonnes in Q1 2026.

This reversal is notable because central banks have provided steady structural demand for bullion through much of the recent gold rally. When that demand softens or turns negative, traders in gold, precious metals, and XAUUSD tend to reassess how much official buying is supporting prices.

Which central banks bought gold in March 2026?

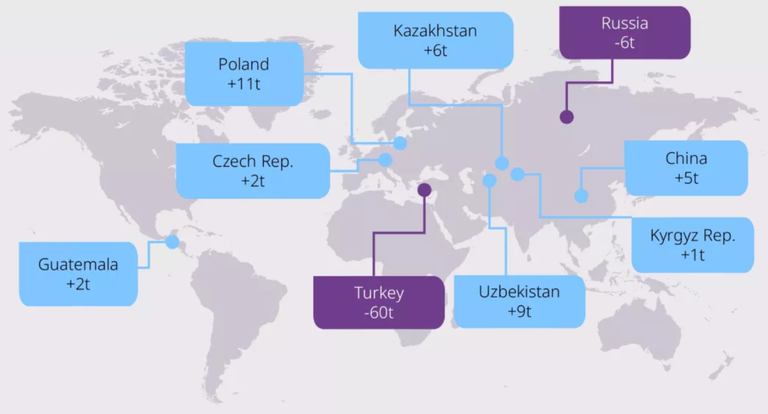

The biggest central bank gold buyers in March 2026 were Poland, Uzbekistan, and Kazakhstan. These countries continued the reserve accumulation trend that has been in place since 2024.

According to Marissa Salim, the National Bank of Poland bought 11 tonnes, making it the largest buyer in March. It was followed by the Central Bank of Uzbekistan with 9 tonnes and the National Bank of Kazakhstan with 6 tonnes.

The People's Bank of China also continued adding to reserves. China extended its buying streak to 17 consecutive months and increased its March pace to 5 tonnes.

Other buyers included Guatemala and the Czech Republic, which each added 2 tonnes in March. The continued accumulation by these central banks shows that while March produced net outflows overall, official-sector interest in gold has not disappeared.

What did Q1 2026 central bank buying look like?

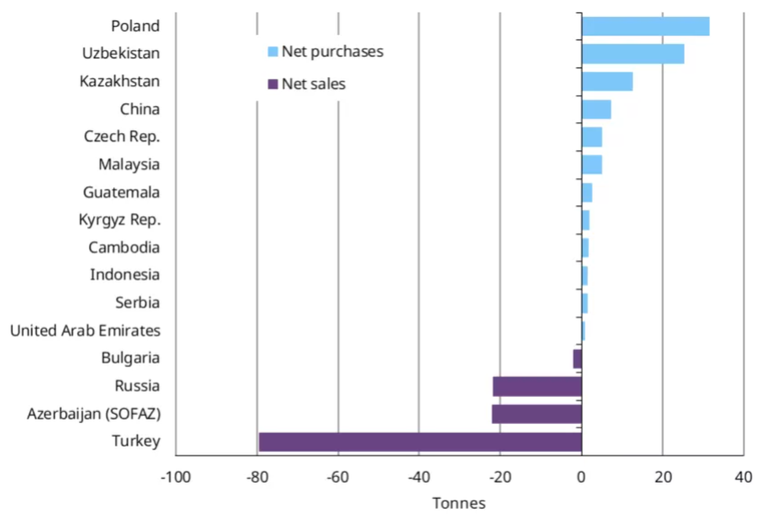

Poland remained the top buyer for the first quarter of 2026 with 31 tonnes purchased. It was followed by Uzbekistan with 25 tonnes, Kazakhstan with 13 tonnes, and China with 7 tonnes.

The Czech Republic, Malaysia, Guatemala, Kyrgyz Republic, Cambodia, Indonesia, and Serbia also reported net buying of one tonne or more in Q1 2026. That broader list suggests central bank gold demand remains geographically diverse even as some countries temporarily sell reserves.

Why did Turkey cut its gold reserves so sharply?

Turkey cut its gold reserves sharply because its central bank used gold sales and gold swap operations to secure U.S. dollar liquidity and support the Turkish lira during a period of market stress. The World Gold Council said Turkey was the largest seller in Q1 2026, with official-sector holdings down 79 tonnes based on available reported data.

Marissa Salim said the bulk of those sales came in March, when the bank used an additional 80 tonnes via gold swaps. Separate reporting in the source article said the Turkish government opened approximately 73 tonnes worth of gold swap positions in March.

The article also said some of the central bank’s bullion was sold during that period, causing a sharp decline in reserves. Those swap operations were used to provide U.S. dollar liquidity as capital outflows accelerated and domestic demand for foreign currency increased.

How far did Turkey’s reserves fall?

Turkey’s gold reserves fell heavily during March. Before the start of the Iran war, the central bank held nearly 830 tonnes of gold.

By the end of March, that figure had dropped by 127 tonnes to 693 tonnes. The source article also said Turkey’s central bank had been the most transparent regarding official reserves, with data showing that its gold holdings declined by more than 118 tonnes in March.

According to reports cited in the source article, this was the biggest drawdown in Turkey’s gold reserves since 2013. The central bank said at the time that it had sold some of its gold while monetizing most of it through swap agreements.

Is Turkey rebuilding its gold reserves now?

Yes, Turkey has started rebuilding its gold reserves as market conditions stabilized. As it unwinds some of the dollar-for-gold swap positions used during peak stress, physical holdings rose to around 730 tonnes as of April 17.

Latest government data showed the bank increased gold reserves by 30.7 tonnes over the past week. That brought total gains to 36.4 tonnes over the past two weeks, reversing part of the earlier drawdown tied to liquidity operations.

The source article said the rebuilding began after the ceasefire between the United States and Iran, which helped stabilize markets, reduced pressure on Turkish assets, and allowed the central bank to restore some bullion holdings.

How does the Middle East war affect central bank gold demand and gold prices?

The war in the Middle East is increasing economic stress and making central bank gold flows more volatile. The source article said sovereign demand remains important to the precious metals market, but some central banks, especially Türkiye’s, have been forced to monetize gold reserves to protect their economies.

The article linked this directly to the ongoing war with Iran. It said the conflict is significantly affecting global economic activity because supply-chain disruptions, especially in the energy market, are pushing inflationary pressures higher.

That creates a complex backdrop for bullion. On one hand, gold benefits from safe-haven demand during geopolitical stress. On the other, countries facing currency pressure or external funding stress may sell or swap gold reserves to raise liquidity, creating temporary supply.

What does this mean for the gold price and Indian investors?

For gold prices, the key message is that central bank demand remains supportive over the longer term, but monthly flows can turn volatile when governments face economic or currency stress. A net sale of 30 tonnes in March 2026 does not erase the broader reserve accumulation trend, but it does show that official-sector demand is no longer a one-way trade every month.

For Indian investors, this matters because global official-sector buying or selling can affect international bullion prices in U.S. dollars per troy ounce, which then feed into domestic prices after accounting for the INR exchange rate, import costs, and local premiums. If central bank sales rise while the rupee strengthens, Indian gold prices may see some relief. If geopolitical risks keep safe-haven demand elevated and the rupee weakens, domestic gold rates could remain firm even if official-sector flows fluctuate.

The next key watchpoint for Indian bullion investors is whether March proves to be a one-off liquidity-driven episode led by Turkey, or the start of a broader change in central bank gold strategy in Q2 2026. Markets will also watch China’s reserve buying pace, Turkey’s reserve rebuilding after April 17, and whether Middle East tensions continue to reshape safe-haven demand for gold.