Gold prices fell during the Iran conflict mainly because crowded positioning, retail participation, profit-taking, and margin-call selling distorted short-term trading, according to Robin Brooks of the Brookings Institution. For Indian investors, that means the recent bullion weakness may reflect market structure and liquidity stress rather than a lasting break in gold’s safe-haven role.

Why did gold prices fall during the Iran conflict?

Gold prices fell because investor positioning had become crowded after a powerful rally, and the buyer base expanded sharply just before the conflict. According to Robin Brooks, Senior Fellow at the Brookings Institution and former Chief Economist at IIF and Chief FX Strategist at Goldman Sachs, the decline in precious metals is better explained by market structure than by a collapse in gold’s safe-haven status.

In an analysis published Wednesday, Brooks said three theories are circulating in markets. The first is that the strong run-up in precious metals before the war pulled in many retail investors who had not previously traded gold, silver, or platinum.

Brooks argued that broader retail participation may have changed how precious metals trade in the short term. In that setup, gold can behave more like a risk asset than a classic safe-haven asset, which helps explain why gold sold off when oil prices spiked and then rallied over the last day or two as expectations of detente increased.

For Indian investors, this matters because XAUUSD can weaken even during geopolitical stress if positioning is stretched. That can increase volatility in domestic bullion prices as global moves feed through to rupee-denominated gold rates.

What three explanations did Robin Brooks give for the precious metals selloff?

Robin Brooks said the selloff in precious metals can be explained by a retail pile-in, profit-taking, and margin-call liquidations. He added that none of these explanations undermines the long-term investment case for gold or the broader debasement trade tied to the U.S. dollar.

How did retail traders influence gold, silver, and platinum?

Retail traders likely entered the market after the sharp rally in late 2025 and early this year. Brooks wrote that the "crazy run-up" in precious metals before the war likely attracted many new investors who did not trade assets like gold before.

He said this broader investor base may make precious metals trade more like risk assets rather than pure safe-haven assets. That view fits the recent pattern in which gold fell when oil prices spiked and then rebounded as hopes of detente emerged.

For Indian bullion buyers, this is a key distinction. A gold price correction during geopolitical stress does not automatically mean Indian demand for portfolio hedges or inflation protection has weakened.

Why would investors take profits in gold?

Investors may have taken profits because many were already sitting on large gains after the rally in late 2025 and early this year. Brooks said rising uncertainty often pushes traders to take chips off the table.

That means the decline in gold does not necessarily signal fading confidence in bullion. It may simply reflect rational profit-booking after a steep advance in gold, silver, and platinum.

For investors in India, profit-taking in global bullion markets can translate into lower or more volatile local prices per 10 grams, though the final move also depends on the rupee and import-related costs.

How did margin calls pressure precious metals?

Margin calls may have forced investors to sell profitable precious metals positions to raise cash. Brooks said rising volatility likely pushed other trades, especially hedge fund positions, into the red.

When that happens, traders often need immediate liquidity. Gold, silver, and platinum can become funding sources because they were among the profitable trades available to sell.

This matters for Indian investors because forced selling can create sharp short-term drops in XAUUSD even when the long-term case for gold remains intact. Rupee moves can either cushion or amplify that impact in the Indian market.

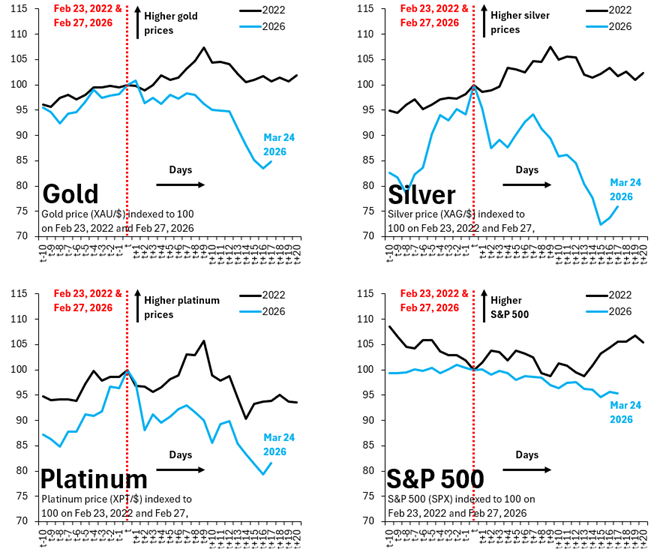

How much have gold, silver, and platinum fallen since the war began?

According to Robin Brooks, all major precious metals have underperformed the broader U.S. equity market since the outbreak of war. He said gold is down 15%, silver is down 25%, and platinum is down 20% since the start of the Iran conflict.

By comparison, the S&P 500 is down 5% over the same period. Brooks said that clear underperformance shows precious metals did not behave as immediate safe-haven winners in this episode.

Does a 5% fall in the S&P 500 count as a true risk-off shock?

Brooks said no, a 5% decline in the S&P 500 hardly qualifies as a major risk-off event. In his view, that means gold’s traditional safe-haven status may not have been fully triggered during this market phase.

He said that supports the idea that recent declines are a vestige of the huge run-up in precious metals prices and positioning. In other words, the selloff may reflect a positioning purge more than a rejection of gold as a safe-haven asset.

For Indian market participants, that distinction is important. A short-term correction in international bullion prices does not automatically mean long-term demand for portfolio hedges, central-bank diversification, or inflation protection has weakened.

What does the Ukraine war comparison tell us about gold?

The comparison with Russia’s invasion of Ukraine in 2022 suggests that war alone does not always trigger a major gold rally. Brooks said the precious metals response after the 2022 invasion was limited, even though the S&P 500 pattern on a similar time scale looks almost identical to the current episode.

That historical comparison makes Brooks lean further toward the positioning-purge explanation. If a previous geopolitical shock also failed to generate a major sustained rally in gold and other precious metals, the current weakness may be less surprising than it first appears.

For investors in India, this means geopolitical headlines alone may not be enough to drive a sustained rise in local gold prices. The rupee, import costs, global positioning, and broader precious-metals flows can all shape what Indian buyers ultimately pay.

Does this selloff mean gold is no longer a safe-haven asset?

No, Brooks explicitly said the recent explanations for the selloff do not invalidate gold’s safe-haven status. He believes the latest price action shows that the buyer base may have broadened, which is why precious metals are displaying atypical behavior right now.

Brooks also pushed back against the idea that the decline disproves the longer-running U.S. dollar debasement trade. His broader point is that short-term price weakness in bullion can coexist with a still-intact long-term case for holding gold.

That view matters in India, where investors often use gold as both a cultural store of value and a financial hedge. If the current move is mainly a positioning reset, Indian investors may want to watch whether global speculative flows stabilize, whether XAUUSD regains momentum, and whether rupee moves alter the domestic price trend.

The key watchpoint now is whether precious metals continue to lag even if volatility stays elevated. If forced selling fades and safe-haven demand reasserts itself, gold could begin trading more in line with its traditional role again.