China’s gold price performance was flat in April, but Chinese gold ETFs and the People’s Bank of China (PBoC) kept buying aggressively. According to Ray Jia, research head for China at the World Gold Council (WGC), this combination shows that investor and official-sector interest in gold remained firm even as wholesale demand weakened and gold jewellery consumption stayed under pressure.

For Indian investors, the update matters because China is one of the world’s largest gold markets. Strong Chinese ETF inflows, sustained central bank buying, and rising imports can influence global gold price, bullion flows, and sentiment in XAUUSD, even when retail demand softens.

What Happened to Gold Prices in China and Globally in April?

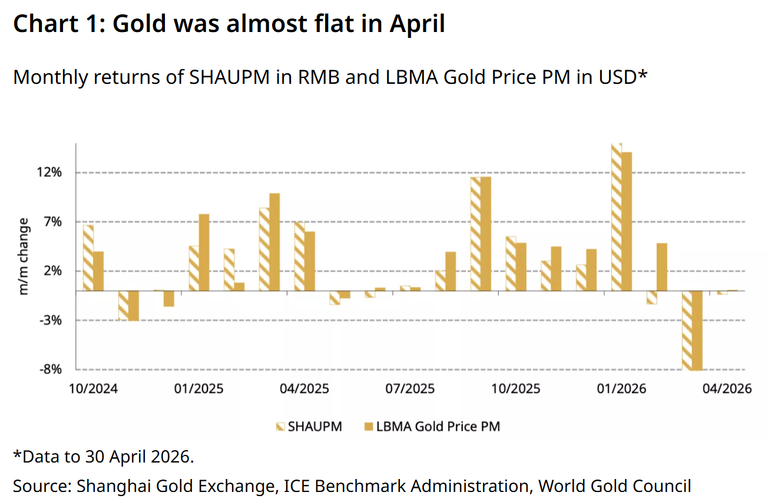

Gold prices moved sideways in April. International and Chinese benchmark prices ended the month almost unchanged, reflecting a market that lacked a clear directional trend.Ray Jia said the LBMA Gold Price PM rose 0.1% in April, while the Shanghai Gold Benchmark Price PM (SHAUPM) fell 0.4%. That means both global and local gold price benchmarks were effectively flat over the month.

Why did gold trade sideways?

Gold first recovered from weakness seen in March, but later gave back those gains. Jia said easing Middle East tensions early in April reduced inflation worries and weighed on bond yields, helping gold rebound.

Later in April, uncertainty around the Strait of Hormuz pushed oil prices higher. That shift reduced expectations for Federal Reserve easing and reversed gold’s earlier gains.

For Indian investors, this pattern is important because global geopolitical shocks and U.S. rate expectations often feed directly into domestic gold rates through international bullion prices and the USD/INR exchange rate.

Why Did Chinese Gold ETFs See Inflows Again?

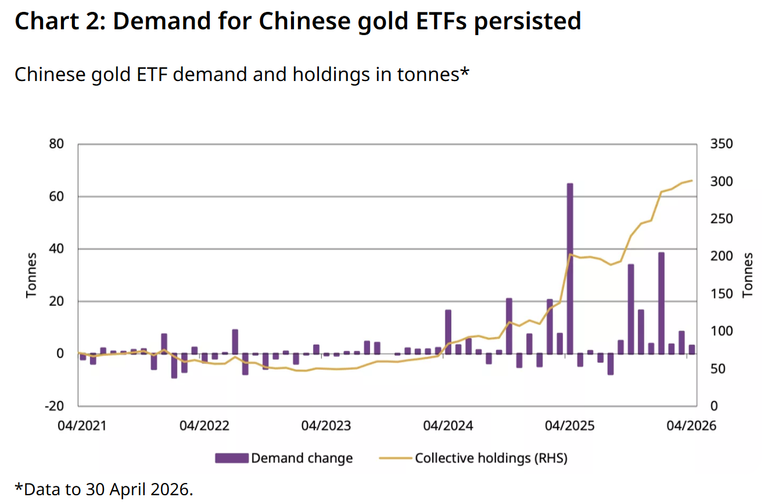

Chinese gold ETFs recorded an eighth straight month of inflows in April, showing that investors continued to use gold as a safe-haven and portfolio diversifier.According to Ray Jia, Chinese gold ETFs attracted RMB3.5 billion (US$498 million) in April. After that monthly expansion, total assets under management (AUM) reached RMB306 billion (US$45 billion), up 1% month-on-month.

How much did holdings increase?

Collective holdings rose by 3 tonnes to 301 tonnes, setting another month-end record. That means ETF investors kept adding exposure even though the local gold price was no longer trending sharply higher.

What drove investor demand?

Jia said global and regional geopolitical tensions and falling local government bond yields supported investor interest in gold. In other words, investors still saw gold as a useful safe-haven asset.However, he also noted that inflows slowed because some investor money may have shifted into the rallying Chinese equity market.

What does the WGC expect next?

The World Gold Council expects local investors to continue allocating to gold ETFs in May, especially as the local gold price has stabilized. Even with a stock market rally, steady prices may help preserve interest in gold as a portfolio hedge.For India, this has a useful parallel. Indian investors also tend to increase allocations to gold ETFs, physical bullion, and sovereign gold-linked products when geopolitical risks stay elevated or when fixed-income yields look less attractive.

How Active Was China’s Gold Futures Market in April?

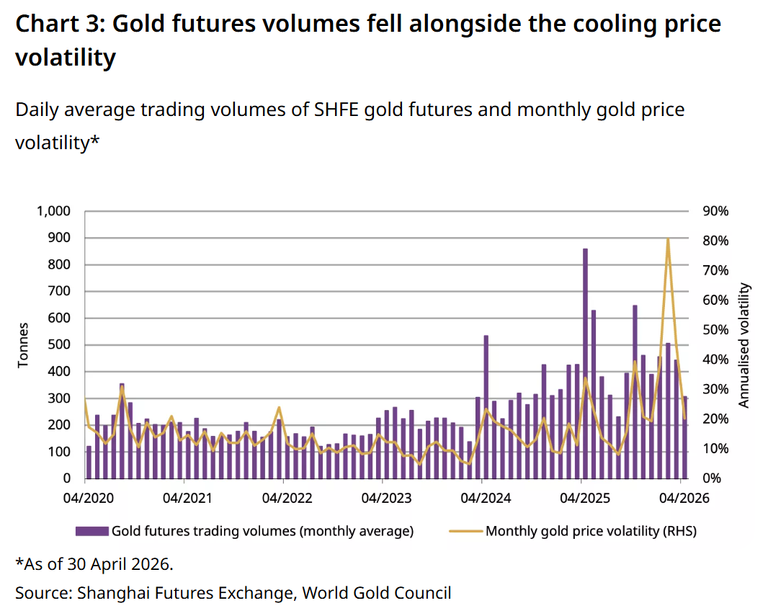

Gold futures trading cooled in April, but activity remained strong by historical standards. That suggests traders became less aggressive, not absent.

Ray Jia wrote that gold futures volumes on the Shanghai Futures Exchange (SHFE) fell 31% month-on-month to 307 tonnes per day. Even after that decline, volumes remained well above the five-year daily average of 265 tonnes.

Why did futures activity decline?

Trader interest weakened because the local stock market strengthened and gold price volatility eased. When prices move in a narrower range and equities rally, speculative futures demand often slows.For bullion traders in India, that is a signal worth watching. Lower futures activity can indicate fading short-term momentum, even if longer-term investment demand for gold remains intact.

Why Did China’s Wholesale Gold Demand Fall?

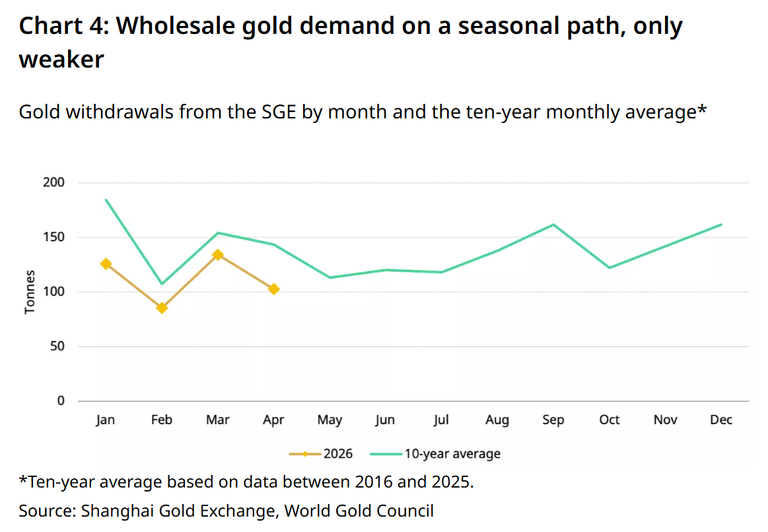

China’s wholesale gold demand fell sharply in April mainly because of seasonal weakness and a continued slowdown in the gold jewellery sector.Gold withdrawals from the Shanghai Gold Exchange (SGE) totalled 103 tonnes in April, down 23% month-on-month. Jia said this follows a normal seasonal pattern, as restocking typically falls in April when gold jewellery consumption enters its traditional Q2 off-season.

Did the Labour Day holiday help demand?

Only marginally. Jia said there was some replenishment ahead of the early-May Labour Day holiday, which has historically supported jewellery sales, but the impact was limited.Consumer spending in China continues to shift toward experiences such as travel, reducing support for jewellery demand.

What happened to bullion demand?

Bullion sales remained healthy, but they cooled from the earlier buying frenzy. Strong equities and easing gold price momentum reduced investor urgency to buy physical gold.How weak was demand on a yearly basis?

April wholesale demand fell 33% year-on-year. However, Jia said the annual comparison was distorted by a high base because April 2025 demand was the highest level since 2018.He added that weaker wholesale demand has still been a broader theme this year, driven mainly by the downturn in the gold jewellery sector.

For Indian investors and jewellers, this trend matters because weak jewellery consumption in China can offset some support from investment demand. That balance can influence the global gold price, especially during key festive and wedding demand periods in Asia.

How Much Gold Did the PBoC Buy in April?

The People’s Bank of China bought 8 tonnes of gold in April, marking its strongest monthly addition in nearly a year and a half.According to Ray Jia, the PBoC reported an 8-tonne gold purchase in April, its 18th consecutive monthly addition and the highest since December 2024.

What are China’s total official gold holdings now?

The latest purchase lifted China’s official gold reserves to 2,322 tonnes. Gold now accounts for 9% of the country’s total official reserves.At the same time, China’s total official reserves rose 2% to US$3.8 trillion.

Why does central bank buying matter for gold prices?

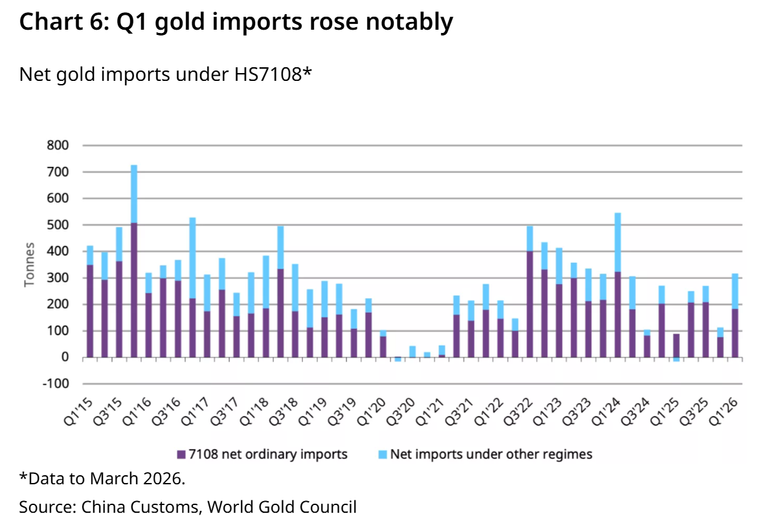

Central bank accumulation supports the long-term bull case for gold because it reflects persistent reserve diversification away from fiat and geopolitical risk exposure. For Indian investors, sustained buying by major central banks such as the PBoC can strengthen the structural floor under global bullion prices.How Strong Were China’s Gold Imports?

China’s gold imports rebounded sharply in March and surged across the first quarter. That points to stronger underlying physical demand than weak jewellery trends alone might suggest.Ray Jia said China imported 143 tonnes of gold on a net basis in March, a 49% month-on-month increase.

What happened in the first quarter?

The March rebound pushed Q1 net gold imports to 316 tonnes. That represented a jump of 182% quarter-on-quarter and 333% year-on-year.What explains the import surge?

Jia said the data reflected robust Chinese gold consumption during Q1. Strong bullion investment offset weak jewellery buying.He also said that a positive local gold price spread throughout the quarter encouraged importers.

This is relevant for Indian readers because Chinese import strength can tighten regional physical supply conditions and influence premiums, especially when Indian festival or wedding demand accelerates.

What Is the Outlook for Gold Demand in China?

The World Gold Council expects Chinese consumer demand for gold to remain weak in the near term, especially in the seasonal off-season for jewellery.Jia said the stabilising gold price may offer some support, but several headwinds remain. Rising investor interest in the local equity market rally, which began in early April, and the lack of a clear gold price trend may continue to discourage bullion investment.

For Indian investors, the key watchpoint is whether Chinese central bank buying and ETF inflows continue to outweigh softer jewellery demand. If official-sector purchases remain strong and geopolitical risks stay elevated, global gold prices could remain supported even if Asian retail demand stays uneven. A sustained move in XAUUSD, shifts in USD/INR, and changes in local Indian premiums will be crucial signals to monitor next.